The BTC Horse Racing Thread

-

@nick-allan said in The BTC Horse Racing Thread:

@john-folan nice one john, does the software have a percentage decrease inplay running feature?

It has a lowest and highest price inrunning against bsp feature so as a simple example you can do lowest price inrunning =50% of bsp(so a dob) 70% of last x runs

-

@john-folan nice one john, does the software have a percentage decrease inplay running feature?

-

@nick-allan working on it

-

I'm interested in purchasing the horse trading software, but in the past I've only really traded lay to back, now I know that you could create a system using the software, but having a look at the set forget strategies there doesn't appear to be one for a lay to back, is there any profitable lay to back strategies available that I could test?

-

@jonathan-jones makes sense that. Less of a problem trading the top few in the price rankings as plenty of dollar there to get in and out.

Stuff like this is great as there are some sharp minds on here and between us all we will soon work out what’s worth bothering with and what isn’t.

Pre race being a prime example. Last 20 minutes there’s enough money to get in and there is no problems trading out the closer to the off you get. Yes you can use the software to target horses to trade pre race. I have one in test at the moment and it is matching the bot exactly. But again I am targeting odds below 20 where the majority of the liquidity is. Upscale able is the new watch word. Pretty irrelevant for straight lays or backs as most things get matched. But especially for inrunning you need to know it’s ok. There is a traded volume filter in the software that should help.

-

@adam said in The BTC Horse Racing Thread:

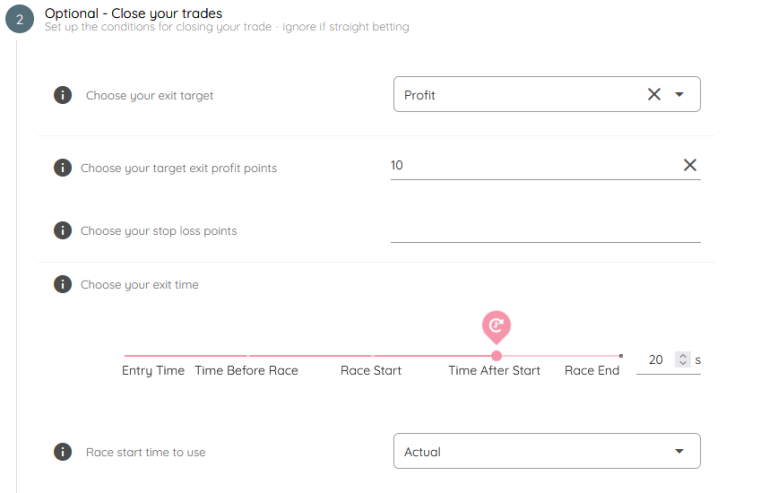

Re your exit settings, your understanding looks right. Just to double check though, you're targeting 10 points profit, which would be 10 x your stake. Is that what you're expecting, or are you expecting 10% of your stake? We had some debate over what the definition of a "point" should be in the early stages of development.

I set it up in the automation the same way i set up the DOB. In the backtester the DOBs are set up at profit = 1, In fairbot this translates to 'odds = 1', so for this its 'odds = 10'. I will check some individual trades to see if i can get a better understanding of what exactly is going on but from the responses it is looking like its the combination of of the general 'randomness' introduced by the 'trade out' compounded by the liquidity gaps on the horses this strategy is targetting.

So, still. I think we all need to look at the strategies we create then take a view based on all the above as to how well real life will conform to the backtest (Probably more accurate saying it that way round than 'backtest conform to real life').

-

@martin said in The BTC Horse Racing Thread:

@john-folan do you have an odds limit on slow horses? I know you scrapped zero on the higher odds being hard to green up on.

Not at the moment. These seem to work ok for some reason. I’m looking at them this week to see if they can’t be refined with different entry points.

-

@john-folan do you have an odds limit on slow horses? I know you scrapped zero on the higher odds being hard to green up on.

-

Todays

Classic Trobs: Dob, Trob or Win if odds are between 3.5-9

Slow Horses. Dob any over 6.0 as close to the off as possible

NONE TODAYFlat Pace. Back to Win if between 2.0-25.0. 4-14 Runners only. Avoid Soft, Heavy and Firm Going

Read the first post on both threads.

Horse Trading Resources

https://forum.betfairtradingcommunity.com/topic/1111/john-s-horse-trading-resourcesBfBotmanager

https://forum.betfairtradingcommunity.com/topic/2915/bfbotmanager-automation-discussion -

@jonathan-jones said in The BTC Horse Racing Thread:

@adam

I know you have betfair tick data but that doesnt mean if you want to exit at a price or time that you will exit at a price or time.Longer priced horses have massive gaps in liquidity so when you add in the inplay delay your chances of getting matched are quite low.

Those things are absolutely true. We're showing you which prices were genuinely reached in the past, but of course throwing your own bets in the mix can have their own influence. And we can't account for whether you manage to execute your own strategy perfectly.

I would just like to point out though that that means something slightly different to "you can't trust that what the backtest shows actually happened"

Unless you can accurately model the effects of the inplay delay along with how much was matched at that price as a proportion of how much was waiting to get matched (not sure you even have that data) and add some magic to account for how much your stake would of influenced that and whewre in the queue your money was i dont think there is that much you can do

Nothing is impossible. When I automated my own scalping strategy, I built in queue position and fill rate estimations, to the extent that it was able to time the simultaneous matching of a back and lay bet with decent accuracy. I'm planning on adding the same enhancements to the horse racing software.

Re your exit settings, your understanding looks right. Just to double check though, you're targeting 10 points profit, which would be 10 x your stake. Is that what you're expecting, or are you expecting 10% of your stake? We had some debate over what the definition of a "point" should be in the early stages of development.

-

@jonathan-jones No trading software can mimic real life exactly. Especially when you are talking about a few ticks here and there, and low liquidity. If I did those rules manually, and you did them manually at the same time as me, I guarantee we'd both have different results.

Due to the way the software works, it will give you an out, which you may not get in real life, especially at the odds you are working with. This is why I've never used big odds in-running. Plenty of systems that look profitable, are not.

The more liquidity, the more accurate this software is, but that also applies when trading for real.

Watch the high odds horses in-running on a ladder interface, and you'll see little liquidity. No software would accurately replicate what would happen in real life with so little money around.

")

-

Break evens on slow horses. I’m going to look at max odds and entry points the next few days. I reckon these can be maximised a fair bit.

Flat pace doing what it’s supposed to. At some point we will hit a 25 winner. They will fly then

-

Nice winner for Mr Zee at 5.7

Better odds than BSP as well

-

@adam

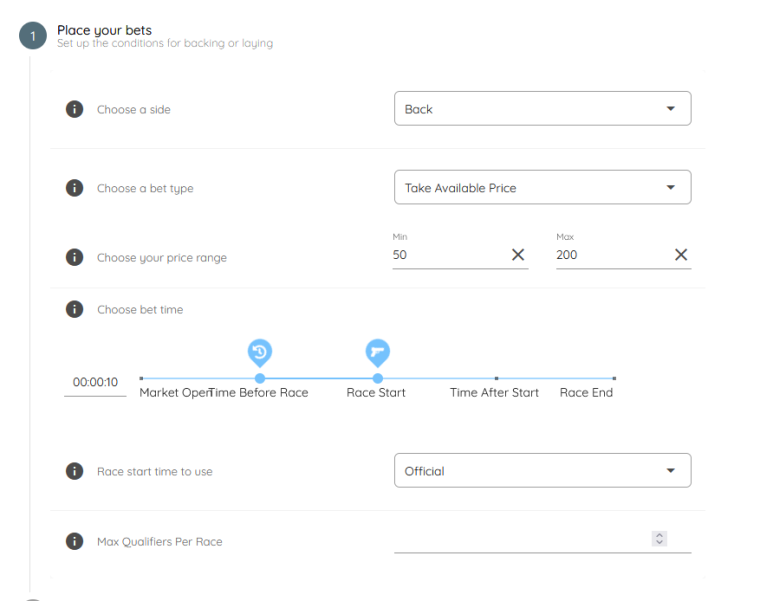

Its possible we are all confused by the exit criteria and my automation is set up wrong. This is my entry criteria:

So, as far as i understand, Back all horses at odds of 50 to 200 from 10 seconds before the official start time to the start time.

This is my exit:

As i understand thats exit at 10 points or 20 seconds after the race goes inplay. I have set that up in automation as a back bet with an offset of 10 points (so the closing lay gets placed as soon as the back is taken) and a 'green/red up all' function which will hedge everything 20 seconds after the race goes inplay (criteria are that there are still bets running) which will repeat 5 times with a 5 second wait. That would pretty much morror how you would do it manually anyway.

Is that correct?

you can easily test hat one yourself. It uses no filter (well, it needs you to add something for it to actually run so i just added courses and select all of them). You will probably be astonished by how profitable the backtester says it is. The last 3 days in the backtester have been profitable. But when run live they all lost.

-

@adam

As i said. It probably sounds like more of a critisism than it actually is. I think the problems are probably down to what i mentioned. I know you have betfair tick data but that doesnt mean if you want to exit at a price or time that you will exit at a price or time. I think this particular strategy (and my variation) make things worse because they target longer prices. Longer priced horses have massive gaps in liquidity so when you add in the inplay delay your chances of getting matched are quite low.Its not that i trust the trading software more. Its just fairbot, and all i have done is set up the exact rules from this strategy in automation. Thats why i wanted to confirm i had understood the exit properly. When you do a green/red up you quite often need to try a few times to get fully out. I am still trying to understand the difference myself but there certainly is one. When traded live with automation (so exactly according to the rules) with this strategy its produced 3 days losses. When backtested the next day its produced 3 days profitable (one day -8 points live, +10 in backtest). Perhaps if it wasnt automated and had a person greening then the result may be more profitable. But, thats not really backtestable either.

I dont know what the solution is (or even if there is one). All i know is the same rules are producing different outcomes. I have seen it to a lesser extent with the DOBs too. You get a few partial matches on the exit (which the backtester always says are full matches) and one occasion where the backtester said i should of been matched on my exit but i wasnt (perhaps my money was at the back of the queue etc). Perhaps its just something we will all end up learning the limitations of. Perhaps low price/higher traded volume horses will produce more accurate results etc.

Unless you can accurately model the effects of the inplay delay along with how much was matched at that price as a proportion of how much was waiting to get matched (not sure you even have that data) and add some magic to account for how much your stake would of influenced that and whewre in the queue your money was i dont think there is that much you can do.

-

@jonathan-jones: Quite a few sweeping statements there, but I'm always keen to find opportunities to improve the software.

Can you maybe share what you think is unreliable about the backtesting? What is it that makes it "near useless" for anything in-play?

Why is it that you can't trust that the data we present actually happened? We do in fact use the actual Betfair prices that were traded, using the actual runner change messages sent by Betfair's streaming API.

You also mentioned that you'd automated it with something else, and it sounds like you trust that method more. Can you share what that is and why you feel it's more reliable?

-

@jonathan-jones thanks for the feedback. I'm not sure if @Adam can take a look and see if there's an issue with back testing the trading out part of the software?

-

@keith

Thats exactly what i thought it would do. I have been automating something similar (Not the same filter but exactly the same trade mechanism) and am seeing the total reverse.The backtest on this one is completely unreliable. 3 days of examples. Backtest shows profits, real time trading shows loss. A massive differnce too, not just a bit. 3 days profit (up to 10 points one day) on backtest but 3 days loss (1 point, 8 points, 6 points) in live testing.

Its not the filter thats the problem, its the implementation. As far as i know Martin never actually traded it, just looked at the backtest with the basic filter and thats not valid as its the backtest thats not reliable.

The software seems fine with simple backs/lays but anything inplay and its near useless, you cant trust that what the backtest shows actually happend. Which isnt as much of a critisism as it sounds and shouldnt be a surprise really. You can never predict how a green/red up will go, particularly with stupid priced horses that have little liquidity.

Forward testing live is still king i think. Even if its just a couple of weeks to confirm the backtest and real life performance match.

-

Thanks for the tag @John-Folan

@Jonathan-Jones the details are in the horse strategy megathread but this is the gist of it:It's a backing system based on horses priced over 50.0 10 seconds before the off. After 5 seconds in play, it will look to hedge the bets with a target of 10 points and if it goes against there's a SL of 0.6 points.

So basically it will green up if it can and has a stop loss if it can't.

To be honest I'm not tracking this one live but @Martin did test it against the basic filter and it did well. -

@nick-terracciano No worries mate. It helps me keep things simple as well